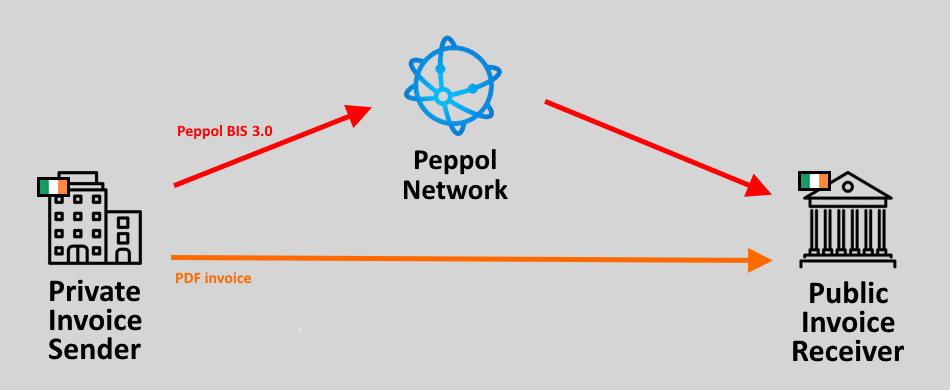

Ireland’s e-invoicing mandate: what to expect by 2028

Irish tax authorities are preparing to implement an e-invoicing mandate ahead of the EU ViDA directive, likely leveraging the Peppol network.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information